This article has been medically reviewed and approved by Dr. Fremlin Dekyi, MD, to support clinical accuracy and patient-friendly education about insurance coverage for weight loss medication. This content is for educational purposes only and does not replace personalized medical advice, insurance benefit verification, or guidance from a licensed healthcare provider.

Does insurance cover weight loss medication?

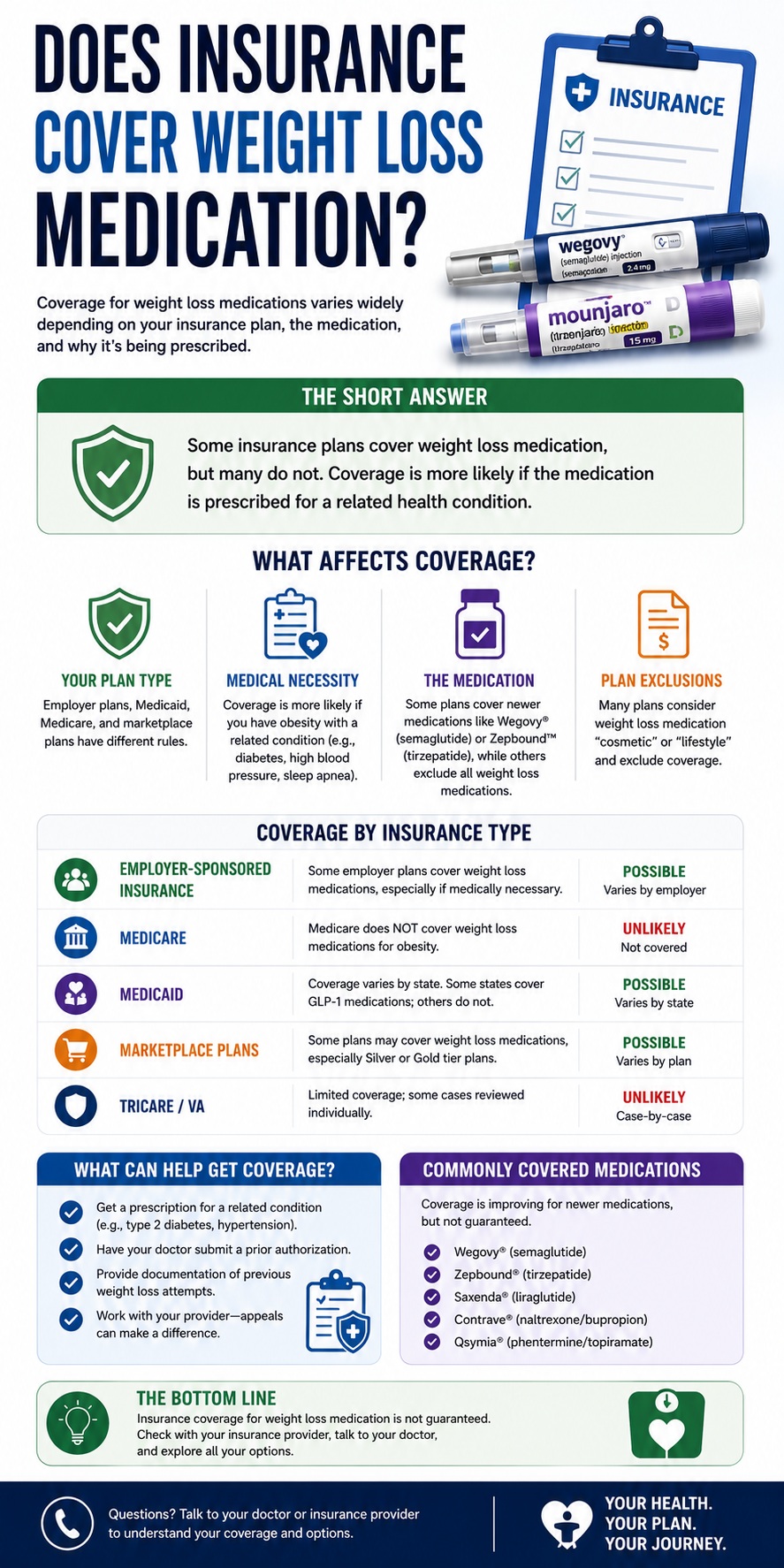

Sometimes. Insurance coverage for weight loss medication depends on the insurance plan, employer benefits, medical history, BMI, weight-related health conditions, the medication prescribed, and prior authorization requirements. Some plans cover medications such as Wegovy, Zepbound, or Saxenda, while others exclude weight loss medications entirely.

One of the first questions patients ask when considering medical weight loss treatment is whether insurance will cover the medication.

It is an important question because newer medications such as Semaglutide and Tirzepatide can be highly effective but may also be expensive without insurance coverage.

There is no universal answer. Coverage varies by insurance carrier, state regulations, employer-sponsored benefits, government programs, and individual plan design. Some patients pay only a small copay, while others face significant out-of-pocket expenses.

This guide explains how insurance coverage works, which medications are commonly covered, common eligibility requirements, and practical steps patients can take to improve the chances of obtaining coverage.

Clinical Evidence: Why Insurance Companies Are Paying Attention

Coverage decisions are influenced by medical evidence, plan design, employer benefits, cost considerations, and long-term health outcomes.

Weight Loss and Health Outcomes

Research consistently shows that meaningful weight loss can improve blood pressure, blood sugar control, cholesterol levels, sleep apnea, cardiovascular risk, mobility, and overall metabolic health.

Even modest weight loss may result in significant health benefits, which is one reason obesity treatment is increasingly viewed through a chronic disease framework.

GLP-1 and GIP Medications

Newer medications such as Semaglutide and Tirzepatide have demonstrated levels of weight loss that were previously difficult to achieve without bariatric surgery.

Many patients lose approximately 10% to 15% of body weight with Semaglutide and approximately 15% to 22% with Tirzepatide in clinical trial settings, although individual results vary.

Why This Matters for Insurance

Health insurers evaluate medical effectiveness, long-term health outcomes, and potential cost savings. If obesity treatment reduces future healthcare costs, insurers and employers may have a stronger incentive to provide coverage.

Why Insurance Coverage Varies So Much

Unlike medications used to treat conditions such as high blood pressure or diabetes, weight loss medications have historically faced inconsistent insurance coverage.

For many years, obesity was viewed primarily as a lifestyle issue rather than a chronic medical condition. As a result, many insurance plans excluded weight management medications altogether.

Today, obesity is increasingly recognized as a chronic disease influenced by genetics, hormones, metabolism, environment, and appetite regulation. This shift has contributed to expanded coverage in some situations, but coverage remains inconsistent.

Which Weight Loss Medications Are Most Commonly Covered?

Coverage changes frequently, but several medications are commonly included in some insurance plans. Coverage is never guaranteed just because a medication appears on a formulary.

Wegovy

Wegovy contains Semaglutide and is FDA-approved specifically for chronic weight management. Some plans cover Wegovy when medical necessity requirements are met, while others exclude it entirely.

Zepbound

Zepbound contains Tirzepatide and is FDA-approved for chronic weight management. Because it is relatively new, coverage policies continue to evolve, and many insurers require prior authorization.

Saxenda, Contrave, and Qsymia

Saxenda has been available longer than many newer GLP-1 medications, and some plans continue to cover it. Contrave combines naltrexone and bupropion, while Qsymia combines phentermine and topiramate. Coverage varies by insurance provider and plan design.

What Is Prior Authorization?

Prior authorization is one of the most common insurance requirements for weight loss medication.

Prior authorization requires healthcare providers to submit documentation showing medical necessity before insurance coverage is approved. The insurance company reviews the information and determines whether the medication meets coverage criteria.

Common Prior Authorization Requirements

Requirements vary, but many plans request similar types of documentation before approving medication coverage.

BMI Thresholds

Many plans require a BMI of 30 or higher, or a BMI of 27 or higher with a weight-related health condition.

Weight-Related Medical Conditions

Examples include hypertension, type 2 diabetes, sleep apnea, prediabetes, high cholesterol, and cardiovascular risk factors. These conditions may strengthen medical necessity arguments.

Previous Weight Loss Attempts

Some plans require documentation that patients have previously attempted diet modification, exercise programs, behavioral interventions, or other supervised approaches before medication coverage is approved.

Which Insurance Plans Are More Likely to Cover Weight Loss Medication?

Coverage depends on the individual plan rather than the insurance company alone. Two patients with the same insurance carrier may have very different coverage if their employer benefits differ.

Employer-Sponsored Insurance

Many patients receive insurance through an employer. Coverage depends largely on benefits selected by the employer. Some employers choose comprehensive obesity treatment benefits, while others choose no obesity medication coverage.

Individual Marketplace Plans

Coverage varies significantly. Some marketplace plans include obesity treatment benefits, while others exclude them. Patients should carefully review plan details before enrollment.

Medicare and Medicaid

Traditional Medicare generally does not provide broad coverage for medications prescribed solely for weight loss, though policies continue to evolve. Medicaid coverage varies by state, with some states providing obesity medication benefits and others offering limited or no coverage.

Why Was My Weight Loss Medication Denied?

Insurance denials are common. A denial does not necessarily mean coverage is impossible.

Common reasons include BMI not meeting plan requirements, missing documentation, excluded benefits, incomplete prior authorization, or step therapy requirements that require patients to try other treatments first.

Can Insurance Decisions Be Appealed?

Yes. Many denials can be appealed. Healthcare providers frequently assist patients by submitting additional medical records, supporting documentation, and appeal letters.

A denial is not always the final decision, especially when the denial was related to missing records, incomplete prior authorization, or documentation that can be clarified.

How Much Does Weight Loss Medication Cost Without Insurance?

Pricing varies considerably by medication type, pharmacy, geographic location, dose, and manufacturer programs.

Without insurance coverage, costs can be substantial. Many patients therefore seek insurance approval, savings programs, or alternative treatment options before starting long-term therapy.

How to Check Whether Your Insurance Covers Weight Loss Medication

Many patients are unsure how to verify benefits. The most reliable approach is to contact the insurance provider directly and work with the healthcare team when documentation or prior authorization is required.

Contact Your Insurance Provider

Ask whether Wegovy, Zepbound, Saxenda, Contrave, or Qsymia is covered, whether prior authorization is required, and what eligibility criteria apply.

Review Your Formulary

The formulary lists medications covered by the plan. Coverage status may change annually, and formulary listing does not always mean a medication will be approved without documentation.

Work With Your Healthcare Provider

Medical offices often help patients navigate insurance requirements, prior authorization requests, appeals, and documentation needs.

Why Coverage Is Expanding

Several factors are driving increased interest in obesity treatment coverage, including growing obesity rates, strong clinical results, employer interest, and research into broader cardiovascular and metabolic benefits.

Employers increasingly recognize that obesity treatment may improve employee health, productivity, absenteeism, and long-term healthcare costs. These trends may influence future coverage decisions.

Does Insurance Cover Semaglutide?

Sometimes. Coverage depends on the specific insurance plan, medical necessity criteria, prior authorization requirements, and whether the prescribed product is FDA-approved for the intended use.

Many plans cover Wegovy under certain circumstances because it is approved for chronic weight management, while others exclude it. Ozempic contains Semaglutide but is FDA-approved for type 2 diabetes, so coverage may be more difficult when it is prescribed solely for weight loss.

Does Insurance Cover Tirzepatide?

Sometimes. Coverage varies considerably. Some plans provide benefits for Zepbound, while others continue evaluating coverage policies as clinical evidence evolves.

Mounjaro contains Tirzepatide and is FDA-approved for type 2 diabetes. Coverage is often easier to obtain when type 2 diabetes is present and medical necessity is documented.

Insurance Coverage by Medication

Not all weight loss medications are treated equally by insurance companies. Coverage often depends on FDA approval status, plan design, employer benefits, and medical necessity requirements.

Does Insurance Cover Wegovy?

Wegovy contains Semaglutide and is one of the most commonly prescribed medications for chronic weight management. Coverage is sometimes available, but it varies significantly depending on the insurance plan, employer-sponsored benefits, state regulations, and individual eligibility requirements.

Because Wegovy is FDA-approved specifically for chronic weight management, some insurance companies are more willing to provide coverage than they are for medications prescribed off-label for weight loss. However, approval is rarely automatic.

Many plans require patients to meet clinical criteria before coverage is granted, including BMI requirements, documentation of obesity-related health risks, previous weight loss attempts, and completion of prior authorization requirements.

Qualifying medical conditions may include high blood pressure, type 2 diabetes, prediabetes, sleep apnea, high cholesterol, and cardiovascular disease.

Many insurers require healthcare providers to submit detailed medical records showing why Wegovy is medically necessary. Even when Wegovy appears on an insurance formulary, prior authorization may still be required before approval is granted.

Patients who receive an initial denial should not assume coverage is impossible. Many approvals occur after healthcare providers submit additional documentation, clarify medical necessity, or complete an appeal process.

Does Insurance Cover Zepbound?

Zepbound contains Tirzepatide and is FDA-approved for chronic weight management. It has become one of the most discussed weight loss medications because of its clinical trial results and substantial weight loss potential.

Some insurance companies have begun adding Zepbound to their formularies, but coverage remains inconsistent across plans. Approval often depends on the insurance plan, employer benefits, medical history, BMI, and coverage policies.

Typical requirements may include a BMI of 30 or greater, or a BMI of 27 or greater with weight-related health conditions, medical necessity documentation, prior authorization approval, and documentation of previous weight loss attempts.

Some insurers may also request weight history, provider notes, laboratory results, and documentation of obesity-related conditions. Conditions such as hypertension, type 2 diabetes, sleep apnea, prediabetes, high cholesterol, or cardiovascular risk factors may strengthen coverage requests.

Because Zepbound is newer than some obesity medications, insurance policies continue to evolve rapidly. Patients who receive a denial should review the denial reason carefully, since providers may be able to submit additional documentation or appeal the decision.

Does Insurance Cover Ozempic?

Ozempic contains Semaglutide, the same active ingredient used in Wegovy. However, insurance coverage for Ozempic often differs because Ozempic is FDA-approved for type 2 diabetes management rather than chronic weight management.

Many insurance companies provide coverage for Ozempic when it is prescribed for patients with type 2 diabetes who meet plan criteria. Coverage may be more difficult when Ozempic is prescribed solely for weight loss.

Insurers frequently review diagnosis codes, medical necessity, diabetes history, previous treatments, and laboratory results. Patients without type 2 diabetes may find that insurers encourage the use of Wegovy rather than Ozempic because Wegovy is specifically approved for obesity treatment.

Coverage policies vary widely between insurance plans. Patients should verify whether Ozempic is covered under their pharmacy benefits and whether prior authorization is required before starting treatment.

Does Insurance Cover Mounjaro?

Mounjaro contains Tirzepatide and is FDA-approved for the treatment of type 2 diabetes. Because of its approval status, insurance coverage is often easier to obtain when a patient has documented type 2 diabetes and meets plan-specific requirements.

Many insurers evaluate diabetes diagnosis, blood sugar history, previous medications, laboratory results, and medical necessity documentation.

Patients seeking Tirzepatide specifically for weight management may find that insurers direct them toward Zepbound instead, since Zepbound is FDA-approved for chronic weight management.

Common requirements may include prior authorization, confirmation of diagnosis, documentation of treatment history, and provider support. As clinical evidence grows, insurers continue updating coverage policies for both Mounjaro and Zepbound.

Patients should review pharmacy benefits carefully and work with their healthcare provider to determine which Tirzepatide product is most appropriate for their clinical situation and insurance coverage options.

State-by-State Medicaid Considerations

Medicaid coverage for weight loss medications varies significantly across the United States. Unlike commercial insurance plans, Medicaid policies are often determined at the state level.

Each state has flexibility regarding covered medications, prior authorization requirements, and obesity treatment policies. A medication covered in one state may not be covered in another.

Because Medicaid policies frequently change, patients should verify benefits directly with their state Medicaid program or healthcare provider.

Employer Coverage Trends

Employer-sponsored insurance is one of the biggest factors influencing coverage. Many large employers choose which benefits are included in their health plans.

Employers are increasingly evaluating obesity treatment benefits because of potential impacts on employee health, productivity, healthcare spending, and absenteeism.

Despite growing interest, some employers remain concerned about medication costs, long-term utilization, and budget impact. This explains why coverage remains inconsistent across employer-sponsored plans.

How Prior Authorization Works Step by Step

Understanding the prior authorization process can help patients avoid delays and frustration.

Step 1: Medical Evaluation

The healthcare provider evaluates BMI, medical history, weight-related conditions, and previous treatment attempts.

Step 2: Prescription Is Written

If appropriate, the provider prescribes a medication such as Wegovy, Zepbound, Saxenda, Contrave, or Qsymia.

Step 3: Insurance Review Begins

The pharmacy or provider submits a prior authorization request. The insurance company reviews diagnosis, BMI, medical necessity, and coverage criteria.

Step 4: Additional Documentation May Be Requested

Insurers may request clinical notes, weight history, lab results, or previous treatment documentation. This is a normal part of the process.

Step 5: Insurance Decision and Ongoing Monitoring

The insurer may approve coverage, request additional information, or deny coverage. Some insurers require periodic reauthorization showing weight loss progress, continued medical necessity, and provider follow-up.

How to Appeal an Insurance Denial

A denial does not necessarily mean the process is over. Many approvals occur after appeal.

The first step is reviewing the denial letter to understand why coverage was denied. Helpful appeal materials may include medical records, provider notes, weight history, and comorbidity documentation.

Most insurance plans provide a formal appeal process. Detailed provider documentation explaining medical necessity, health risks, and previous treatment failures may strengthen the case for coverage.

Savings Cards and Manufacturer Programs

Patients without insurance coverage may still have options. Many pharmaceutical manufacturers offer savings programs, although eligibility rules vary.

Eligible patients may qualify for reduced copays, temporary discounts, promotional savings, or patient assistance programs. Savings offers can change based on manufacturer policies, medication availability, and regulatory requirements.

Paying Out of Pocket

Some patients choose to pay directly for treatment. Potential advantages include immediate access, fewer insurance delays, and no prior authorization requirements.

Out-of-pocket costs can be substantial. Patients should consider monthly medication expenses, long-term affordability, and ongoing follow-up care before beginning treatment.

Before starting therapy, patients should evaluate insurance options, savings programs, and long-term treatment goals to help avoid interruptions in care.

What Improves Your Chances of Coverage?

Several factors may strengthen approval requests, including accurate documentation, meeting BMI criteria, weight-related conditions, and provider support.

Comprehensive medical records, accurate BMI documentation, history of previous weight loss attempts, and documentation of conditions such as hypertension, diabetes, sleep apnea, or high cholesterol may support medical necessity.

Doko Medical Provider Insights

At Doko Medical, one of the most common questions patients ask is whether insurance will cover weight loss medication. The answer often depends on the specific insurance plan rather than the medication alone.

Successful coverage requests typically involve accurate BMI documentation, thorough medical records, documentation of weight-related health conditions, and careful completion of prior authorization requirements.

Patients are often surprised to learn that insurance approval is possible even after an initial denial. Ongoing communication between patients, providers, pharmacies, and insurance companies can be valuable.

Because coverage policies change frequently, individualized insurance verification remains an important part of the treatment process.

Key insurance coverage takeaways

- Insurance coverage for weight loss medication depends on the plan, employer benefits, BMI, diagnosis, medication, and documentation.

- Prior authorization is common for medications such as Wegovy, Zepbound, Saxenda, Contrave, and Qsymia.

- Coverage may be easier when FDA-approved indications and medical necessity criteria are clearly met.

- Denials can sometimes be appealed with stronger documentation from the healthcare provider.

- Patients should verify benefits directly with their insurance carrier or healthcare team before starting treatment.

Use consultation to turn search intent into a real treatment decision

Patients usually get more value from medical review, fit assessment, and follow-up planning than from choosing a medication based only on headlines or social posts.

Frequently asked questions

Related weight loss resources

Sources

- FDA Wegovy Prescribing Information

- FDA Zepbound Prescribing Information

- NIDDK: Prescription Medications to Treat Overweight and Obesity

- NIH / NHLBI: Overweight and Obesity Resources

- American Diabetes Association Standards of Care in Diabetes

- CMS (Centers for Medicare & Medicaid Services): Prescription Drug Coverage