This article has been medically reviewed and approved by Dr. Fremlin Dekyi, MD, to support clinical accuracy and patient-friendly education about Zepbound insurance coverage. This content is for educational purposes only and does not replace personalized medical advice, insurance benefit verification, or guidance from a licensed healthcare provider.

Does insurance cover Zepbound in 2026?

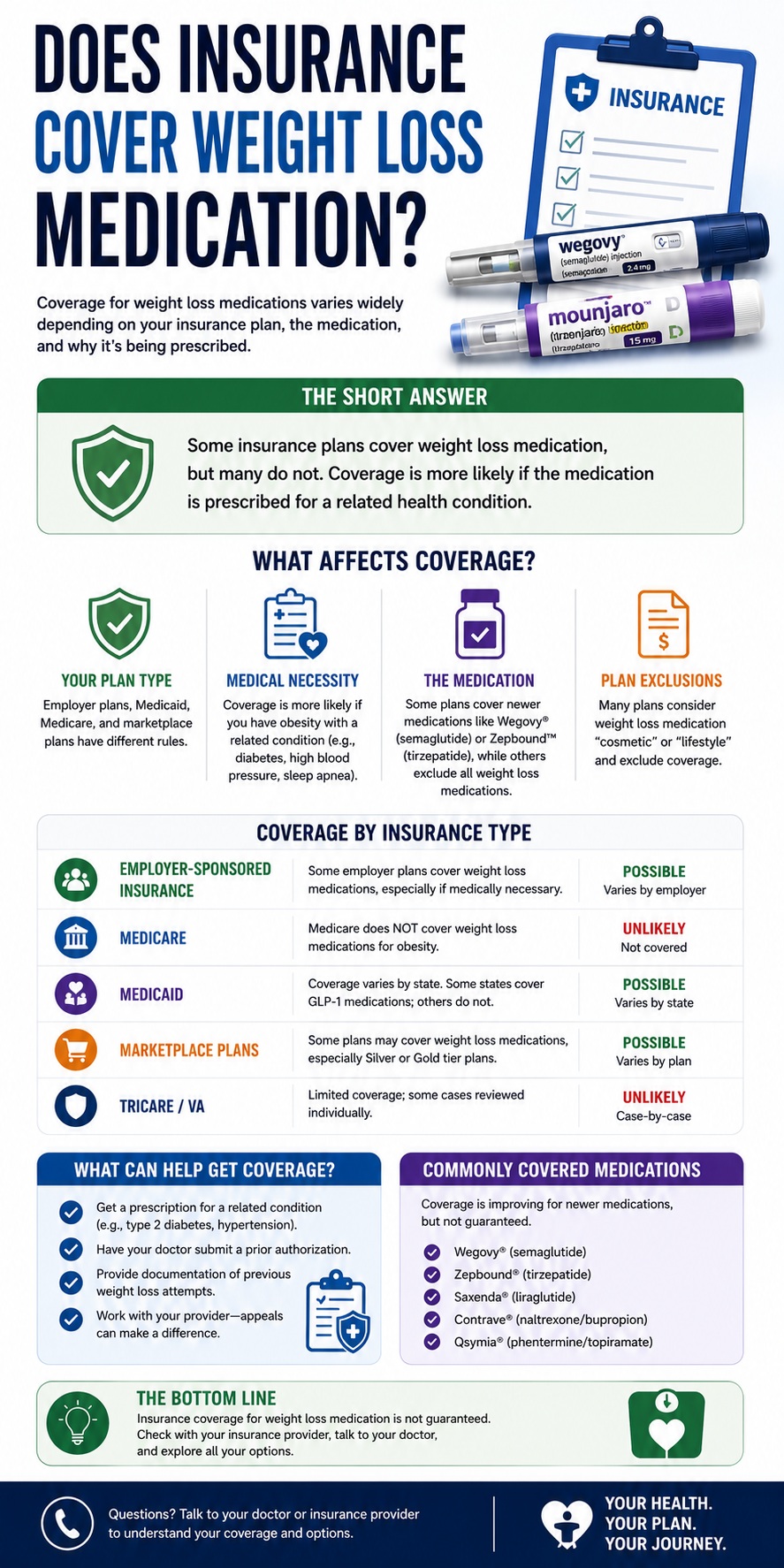

Insurance may cover Zepbound in 2026, but coverage depends on the health plan, employer benefits, medical history, BMI, and clinical requirements. Many commercial plans offer some coverage for eligible patients, though prior authorization is commonly required.

Coverage varies by plan. Eligible patients may significantly reduce their out-of-pocket cost when coverage is approved, but the insurer may require medical documentation before it agrees to pay.

This guide explains the evidence behind Zepbound, the plans that may cover it, common approval criteria, expected costs, and what patients can do after a denial.

Clinical Evidence: Does Zepbound Actually Work?

A growing body of clinical evidence supporting tirzepatide is one reason insurers are evaluating coverage for Zepbound.

Evidence from SURMOUNT-1

The SURMOUNT-1 trial evaluated tirzepatide in adults with obesity or overweight without diabetes. Participants receiving tirzepatide experienced substantially greater weight loss than those receiving placebo.

The study also reported improvements in waist circumference and metabolic health measures. Individual results vary, and medication is intended to be used with reduced-calorie nutrition and increased physical activity.

- Substantial average weight reduction in trial participants

- Improvement in waist circumference

- Improvement in several metabolic health measures

- Weight reduction sustained during continued treatment

What Is Zepbound?

Zepbound (tirzepatide) is an FDA-approved prescription medication for chronic weight management in eligible adults with obesity or overweight and at least one weight-related condition.

It is a GIP and GLP-1 receptor agonist. It can help regulate appetite, increase fullness, slow stomach emptying, and reduce calorie intake. Tirzepatide is also the active ingredient in Mounjaro, which is approved for type 2 diabetes.

Which Types of Insurance May Cover Zepbound?

Coverage is not universal and depends on the benefits included in the individual plan.

Commercial Employer-Sponsored Plans

Employer-sponsored plans are among the most likely to include Zepbound coverage. Coverage depends on employer benefit choices, pharmacy benefit policies, medical necessity rules, and prior authorization criteria. Some employers exclude anti-obesity medications entirely.

Individual Marketplace Plans

ACA marketplace coverage varies by state, carrier, and plan. Patients should check the current prescription formulary and coverage criteria.

Medicare

Medicare coverage rules for anti-obesity medications are limited and continue to evolve. Patients should verify current benefits directly with their plan and discuss covered alternatives with their clinician.

Medicaid

Medicaid coverage varies by state. Some state programs cover anti-obesity medications while others impose restrictions or exclusions.

Why Insurance Companies Require Prior Authorization

Prior authorization is a review the insurer performs before agreeing to pay for a medication. For Zepbound, the plan may use it to confirm eligibility, medical necessity, consideration of alternatives, and alignment with its clinical criteria.

What Is Included in a Zepbound Prior Authorization?

A complete submission often includes the following information.

Patient and Diagnosis Information

The request may include height, weight, BMI, weight history, medical history, and documentation of obesity or overweight.

Weight-Related Conditions

Relevant conditions may include hypertension, sleep apnea, prediabetes, type 2 diabetes, dyslipidemia, or cardiovascular risk factors.

Previous Weight Loss Attempts

Plans may ask for evidence of previous nutrition, exercise, behavioral, or structured lifestyle interventions.

Provider Documentation

The prescribing clinician typically explains why Zepbound is medically appropriate. Complete and accurate documentation may reduce avoidable delays.

Who May Qualify for Insurance-Covered Zepbound?

Criteria vary, but many plans use requirements similar to the FDA-approved indication.

BMI of 30 or Higher

Adults with obesity may qualify based on BMI, subject to the plan’s additional requirements.

BMI of 27 or Higher With a Weight-Related Condition

Adults with overweight may qualify when they also have a condition such as hypertension, sleep apnea, prediabetes, or dyslipidemia.

Medical Necessity

Meeting a BMI threshold does not guarantee approval. The insurer may also assess diagnosis, benefit exclusions, prior treatment, and clinical appropriateness.

Common Reasons Zepbound Coverage Is Denied

Common reasons include a plan-wide weight loss medication exclusion, missing records, failure to meet the plan’s BMI criteria, incomplete prior authorization, or unmet step-therapy requirements. A denial may be appealable.

How Much Does Zepbound Cost With Insurance?

The patient cost depends on the plan, deductible, medication tier, copay or coinsurance, and pharmacy network. Some covered patients may have a relatively low copay, while others may owe more before meeting a deductible.

Benefits and prices change. Patients should confirm the current amount with the insurer and dispensing pharmacy rather than relying on a general estimate.

How Much Does Zepbound Cost Without Insurance?

Without coverage, out-of-pocket costs can be substantial and may vary by pharmacy, dose, manufacturer program eligibility, and current pricing. Patients should verify current pricing and assess long-term affordability before starting treatment.

Which Insurance Companies May Cover Zepbound?

Depending on the specific plan, coverage may be available through Aetna, Cigna, UnitedHealthcare, Blue Cross Blue Shield organizations, Humana, and regional insurers.

Coverage depends on the plan—not merely the company name. Two members insured by the same carrier can have different benefits because of employer choices or plan design.

How to Check Your Zepbound Coverage

Use the current plan documents and ask direct, medication-specific questions.

Step 1: Review the Formulary

Search for Zepbound in the plan’s current prescription drug list.

Step 2: Check Restrictions

Look for prior authorization, step therapy, quantity limits, and anti-obesity medication exclusions.

Step 3: Contact Member Services

Ask whether Zepbound is covered, its tier, approval requirements, and expected copay or coinsurance.

Step 4: Speak With Your Provider

A healthcare provider can evaluate clinical eligibility and prepare the documentation required by the plan.

Zepbound Prior Authorization: Step-by-Step Approval Process

For many patients, obtaining insurance coverage for Zepbound requires prior authorization. Understanding each stage can help patients and providers prepare complete records and respond without unnecessary delay.

Step 1: Medical Evaluation

A licensed provider reviews current weight and BMI, medical history, weight-related conditions, previous weight loss attempts, current medications, treatment goals, and whether Zepbound is clinically appropriate.

Step 2: Documentation Collection

The care team gathers supporting records. Complete, current documentation can reduce preventable delays.

- Height, weight, and BMI

- Obesity diagnosis and relevant comorbidities

- Previous weight-management programs

- Laboratory results when clinically relevant

Step 3: Prior Authorization Submission

The provider submits clinical notes, diagnosis codes, BMI documentation, a medical-necessity explanation, and evidence of previous weight loss efforts through the insurer’s required process.

Step 4: Insurance Review

The insurer checks formulary coverage, medication exclusions, BMI and comorbidity criteria, and any step-therapy requirements.

Step 5: Additional Information Requests

The insurer may request updated weight records, more provider notes, confirmation of previous treatments, or clarification of medical necessity. Prompt responses can keep the review moving.

Step 6: Approval, Conditional Approval, or Denial

Approval permits filling the prescription under plan benefits. Conditional approval may require later reauthorization. A denial means the request did not meet current requirements or the benefit is excluded.

Step 7: Appeals Process

When appeal rights are available, the response may include additional records, updated BMI information, relevant diagnoses, and a provider letter. An appeal does not guarantee approval.

Step 8: Ongoing Reauthorization

Some plans periodically request evidence of continued use, clinical benefit, medical supervision, or adherence to treatment recommendations. Knowing renewal rules early may prevent interruptions.

Zepbound vs Wegovy Insurance Coverage

Both medications may be covered for eligible patients, but approval criteria, formulary placement, and patient costs are not always identical. Coverage for one does not guarantee coverage for the other.

Similarities in Coverage Requirements

Plans commonly use prior authorization, BMI thresholds, medical necessity review, documentation of weight-related conditions, and evidence of previous weight loss efforts for both medications.

Formulary and Approval Differences

A plan may prefer one medication, require less documentation for one, or apply different step-therapy rules. Formularies can change.

Availability and Plan Negotiations

Drug availability, manufacturer agreements, and pharmacy-benefit negotiations may influence preferred status.

Cost Differences

Costs can differ because of formulary tiers, copays, coinsurance, deductibles, pharmacy networks, and savings-program eligibility.

Which Medication Is Easier to Get Covered?

There is no universal answer. Patients should verify current plan requirements and discuss clinical fit with their provider.

Illustrative Zepbound Coverage Scenarios

These hypothetical examples show how eligibility, documentation, and plan design can lead to different decisions. They are educational scenarios, not identifiable patients or guarantees of coverage.

Scenario 1: Employer Plan Approval

An adult with a BMI of 36 and hypertension has an employer plan covering anti-obesity medication. BMI, blood-pressure, and weight-management records support the request.

Scenario 2: Denial Followed by Appeal

An adult with a BMI of 32 and sleep apnea receives a denial for incomplete records. The appeal adds diagnosis records, clinical notes, and a medical-necessity letter.

Scenario 3: Plan-Wide Exclusion

An adult with a BMI of 34 meets clinical prescribing criteria, but the employer plan excludes anti-obesity medications. Clinical eligibility alone does not create coverage.

Scenario 4: Marketplace Plan Review

An adult with a BMI of 29 and prediabetes has a plan covering obesity medication for qualifying members. The insurer reviews prior authorization records and relevant laboratory results.

What Happens After Prior Authorization Is Submitted?

The insurer reviews eligibility, medical necessity, and supporting records. It may approve the request, ask for more information, or deny it. Decisions may take several business days or longer when additional documentation is required.

Can You Appeal a Zepbound Denial?

Yes. An appeal may include additional medical records, updated BMI information, evidence of a weight-related condition, and a provider letter explaining medical necessity. Approval is not guaranteed, but a well-documented appeal may address the reason for denial.

Is Zepbound Worth It If Insurance Covers It?

For an eligible patient, coverage may make treatment more affordable. Potential benefits can include meaningful weight loss and improvement in metabolic health or obesity-related risks. The decision should be made with a qualified clinician after reviewing benefits, risks, contraindications, and long-term treatment needs.

Aetna Zepbound Coverage

Aetna coverage depends on the plan and formulary selected by an employer or policyholder. Plans with anti-obesity medication benefits may require prior authorization, BMI documentation, medical necessity review, and evidence of previous weight loss efforts.

- BMI of 30 or higher may meet one part of the criteria.

- BMI of 27 or higher may qualify when a weight-related condition is present.

- Hypertension, sleep apnea, prediabetes, type 2 diabetes, or high cholesterol may be relevant conditions.

- Members should verify whether anti-obesity medications are included in their pharmacy benefit.

Blue Cross Blue Shield (BCBS) Zepbound Coverage

Blue Cross Blue Shield operates through independent regional organizations, so coverage varies significantly. Some BCBS plans cover obesity treatment while others exclude weight loss medications.

- Prior authorization may apply.

- Step therapy may apply.

- Employer-specific exclusions may apply.

- Quantity limits may apply.

UnitedHealthcare (UHC) Zepbound Coverage

Some UnitedHealthcare plans include obesity treatment benefits, but requirements vary. A plan may request BMI verification, documentation of weight-related conditions, prior weight loss attempts, or participation in a lifestyle program.

- Confirm current formulary status.

- Ask for the exact prior authorization criteria.

- Confirm the copay or coinsurance.

- Check how the deductible affects the expected cost.

Cigna Zepbound Coverage

Cigna coverage depends heavily on the employer benefit package or individual plan. When weight loss medications are included, plans may require clinical records, prior authorization, BMI verification, and medical necessity review. A provider can help submit documentation that addresses the plan’s criteria.

Employer-Sponsored Plans and Zepbound

Employer-sponsored coverage is a major source of Zepbound benefits in the United States. Employers select benefit packages and may choose whether to include anti-obesity medications.

Why Employers May Expand Coverage

Obesity is associated with diabetes, hypertension, cardiovascular disease, sleep apnea, joint disorders, and other health burdens. Some employers view evidence-based obesity treatment as a long-term investment in workforce health.

The Financial Impact of Obesity

Obesity-related healthcare needs can create substantial annual costs through emergency visits, hospital admissions, diabetes care, cardiovascular treatment, and surgical procedures.

Some employers therefore evaluate obesity treatment medications not only as a pharmacy expense, but also as a potential way to improve employee health and reduce future healthcare use. Actual savings vary and are not guaranteed.

- Emergency room visits

- Hospital admissions

- Diabetes medications and care

- Cardiovascular treatments

- Surgical procedures

Why Some Employers Exclude Zepbound

Common reasons include medication cost, budget limitations, rising pharmacy expenses, and uncertainty about long-term utilization.

What Employees Can Do

Employees can speak with Human Resources, request obesity treatment benefits, use benefits feedback channels, and compare options during enrollment. Employers commonly reevaluate benefits annually.

How to Improve Your Chances of Approval

Approval is not guaranteed, but accurate and complete records can prevent avoidable denials.

Maintain Accurate Medical Records

Records should include current weight, BMI, weight history, diagnoses, and relevant comorbid conditions.

Document Previous Weight Loss Attempts

Record nutrition changes, exercise programs, behavioral interventions, and structured programs when the insurer requests this history.

Work With an Experienced Provider

A provider familiar with obesity care and prior authorization can help submit complete forms and respond to insurer requests.

Respond Promptly

Delays often occur when a plan requests more information. Prompt responses can keep the review moving.

What If Insurance Does Not Cover Zepbound?

Patients may appeal a denial, explore covered weight-management benefits or alternative treatments, and compare plan choices during a future enrollment period. An appeal may include updated BMI information, relevant diagnoses, medical records, clinical evidence, and a provider letter of medical necessity.

Future Outlook for Zepbound Coverage

Coverage is likely to keep changing as new clinical evidence emerges, obesity is increasingly treated as a chronic disease, employers assess long-term health costs, and patient demand grows. These trends may encourage broader coverage, but they do not guarantee that a particular plan will add the medication.

Key Zepbound coverage takeaways

- Coverage depends on the specific plan and employer benefit design.

- Prior authorization and medical documentation are common.

- Many plans use BMI 30+, or BMI 27+ with a qualifying condition, as part of their criteria.

- A denial may be appealed with records that directly address the insurer’s reason.

- Current benefits and costs should always be verified with the insurer and pharmacy.

- Whether Zepbound is on the current formulary.

- Whether the plan excludes anti-obesity medications.

- The required BMI and qualifying conditions.

- Prior authorization, step therapy, and reauthorization rules.

- Copay, coinsurance, deductible, pharmacy network, and appeal rights.

Use consultation to turn search intent into a real treatment decision

Patients usually get more value from medical review, fit assessment, and follow-up planning than from choosing a medication based only on headlines or social posts.